Old Pension Scheme (OPS) 2025 & Latest Updates

Rakhal das

Rakhal das

Old Pension Scheme (OPS): Complete Guide 2025

Introduction

The Old Pension Scheme (OPS) is a government-backed retirement plan that was available to central and state government employees in India before 1 January 2004. It guaranteed a fixed lifetime pension to retired employees, based on their last drawn salary, without requiring any employee contribution during their service period.

After 2004, the New Pension Scheme (NPS) replaced OPS for most new recruits, but OPS remains a widely discussed topic due to its benefits, security, and political significance. Some states have even started reverting to OPS for their employees.

Key Features of the Old Pension Scheme (OPS)

| Feature | Details |

|---|---|

| Applicability | Central & state government employees who joined service before 01.01.2004 |

| Contribution | No employee contribution required |

| Pension Amount | 50% of the last drawn basic pay + DA (Dearness Allowance) |

| Dearness Relief | Pension increases with DA revisions, providing inflation protection |

| Family Pension | Provided to the dependent family members after the employee’s death |

| Gratuity | Eligible for retirement gratuity and death gratuity |

| Tax Benefits | Pension income is taxable, but certain exemptions apply |

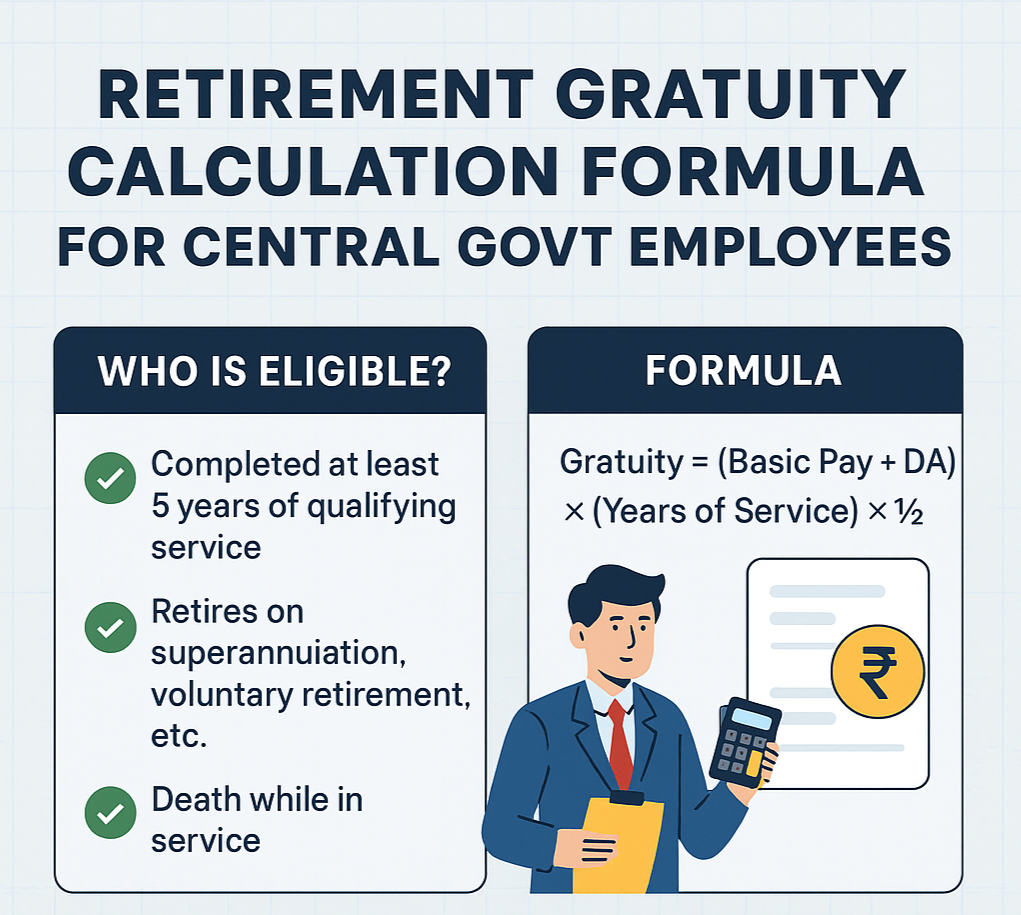

Pension Calculation under OPS

The pension amount is calculated using this formula:

Pension = (Last drawn basic salary + DA) × 50%

For example:

If the last drawn basic salary is 70,000 and DA is ₹20,000 →

Total = 90,000

Pension = 90,000 × 50% = 45,000 per month

Additionally, pensioners receive DA hikes twice a year, just like serving employees.

Benefits of the Old Pension Scheme

- Guaranteed Pension – Fixed pension for life ensures financial stability after retirement.

- Inflation Protection – DA-linked pension increases keep pace with cost of living.

- Family Pension Security – Ensures support for spouse/dependents after the employee’s death.

- No Contribution Burden – Employees don’t need to invest any portion of their salary.

- Gratuity & Other Benefits – Lump sum payment at retirement adds extra security.

Drawbacks of OPS

- High Fiscal Burden – Government bears the entire pension cost, affecting budget sustainability.

- No Individual Pension Fund – Pension is not linked to actual savings or investments.

- Demographic Pressure – Increasing life expectancy means governments must pay pensions for longer durations.

- Not Portable – OPS is tied to government service; private sector employees cannot avail it.

OPS vs NPS: A Quick Comparison

| Feature | OPS (Old Pension Scheme) | NPS (New Pension Scheme) |

|---|---|---|

| Start Date | Before 2004 | Implemented from 2004 |

| Contribution | No employee contribution | Employee & govt both contribute |

| Pension | Fixed 50% of last salary | Market-linked, depends on corpus |

| DA Benefit | Yes, pension revised with DA | DA not applicable |

| Portability | Limited | Portable across sectors |

| Risk | Government bears risk | Market risk shared by employee |

OPS Revival: Recent Developments

Several states have recently announced a return to the Old Pension Scheme due to employee demands and political promises.

States that have announced or implemented OPS revival include:

- Rajasthan

- Chhattisgarh

- Himachal Pradesh

- Punjab

- Jharkhand

The Central Government, however, continues to follow NPS for new recruits. The issue remains a major point of debate between employee unions, economists, and policymakers.

Who is Eligible for OPS Today?

- Central and state government employees who joined service before 01.01.2004

- Employees of states that have officially revived OPS (subject to state rules)

- Certain specific categories like armed forces personnel, who still have separate pension rules

Conclusion

The Old Pension Scheme (OPS) remains popular among government employees for its security, stability, and inflation protection. However, it also poses fiscal challenges for governments.

As debates over OPS vs NPS continue, employees must stay informed about their pension entitlements, state policies, and long-term financial planning.

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.png)

.png)