8th CPC Minimum Pension Calculation 2026: Expected Fitment Factor, Revised Pension Formula

.png)

Rakhal das

Rakhal das

8th CPC Minimum Pension Calculation 2026: Expected Fitment Factor, Revised Pension Formula

The upcoming 8th CPC is eagerly awaited by central government employees and pensioners in India because it promises revision of salaries, allowances, and pensions. This article focuses specifically on how the minimum pension could be calculated under the 8th CPC — the key components, the estimated figures, how to compute, and the things pensioners should keep in mind.

1. Background: What is the 8th CPC and why is pension relevant?

The Pay Commission in India is a periodic committee constituted by the central government to review and recommend changes in salaries and pensions of central government employees and pensioners. The 7th CPC was implemented for central government employees and pensioners, and now the 8th CPC is on the anvil.

For pensioners, the Pay Commission is relevant because one outcome is the re-computation of pension — either by applying a new multiplier (fitment factor) to the existing pension, or by revising minimum pension levels, commutation factors, family pension, etc. For example, early media reports project a jump in the minimum pension under the 8th CPC from about ₹9,000 to about ₹25,740 if a multiplier around 2.86 is used.

2. Current status: What is the minimum pension now and what are the projections?

Current minimum pension

Under the existing regime (i.e., after the 7th CPC and current pension rules), the minimum pension for central government pensioners is ₹9,000 per month (as often referred).

Projected minimum pension under 8th CPC

Media and analysts estimate that under the 8th CPC, if a fitment factor of around 2.28 to 2.86 is adopted for pension revision, then the minimum pension could rise substantially. For instance:

- With a multiplier ≈ 2.86: Minimum pension of ~ ₹25,740.

- Some estimates use lower multiplier (~1.92) for some categories, leading to lower values.

- Analysts say the minimum basic pay of employees under 8th CPC may move from the current ~₹18,000 to ₹30,000-plus or even higher, which will have knock-on effect for pensions.

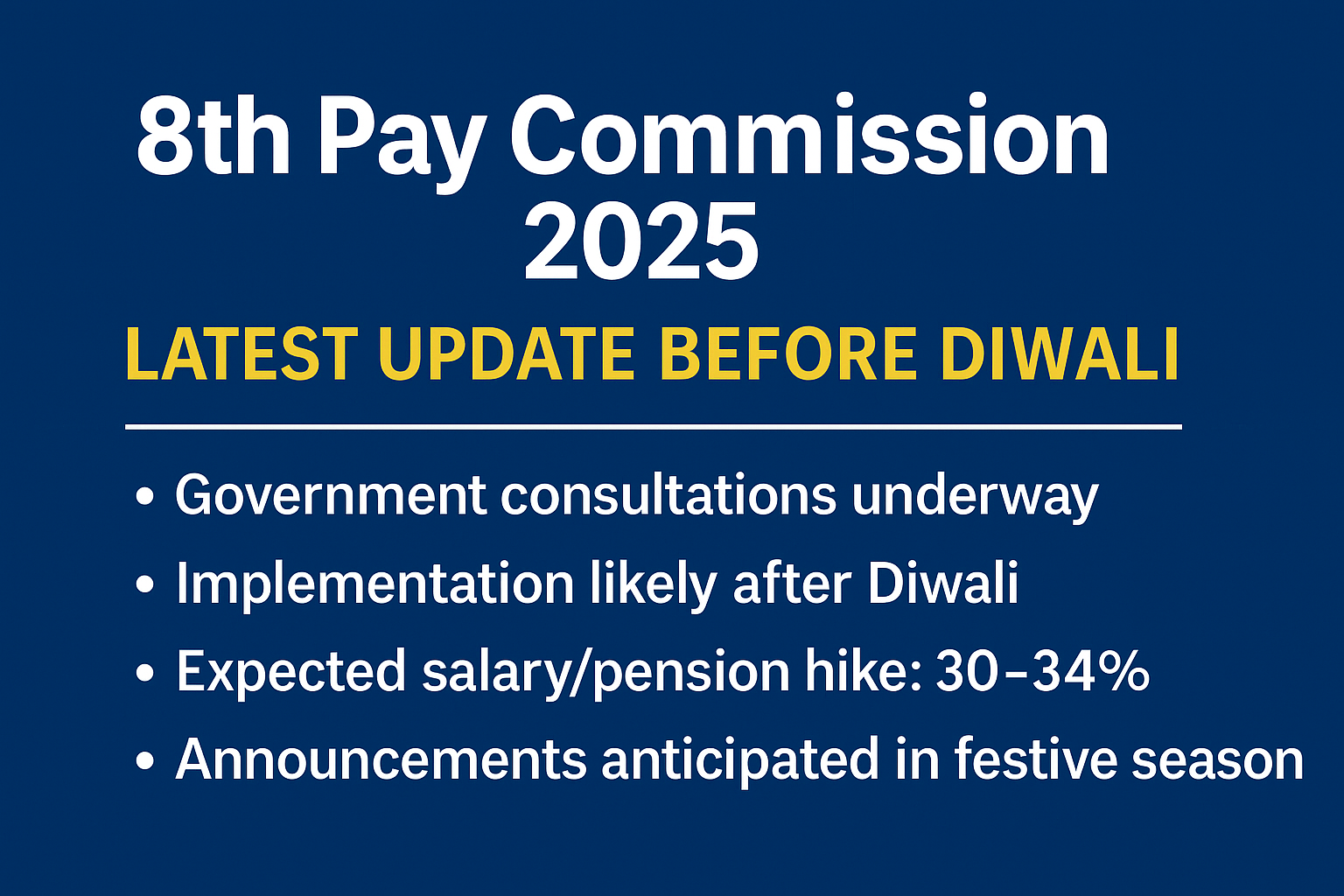

It must be stressed: these are estimates, since the 8th CPC’s terms of reference, multiplier for pensions, etc., have not yet been formally notified.

3. Key components/terms you must know for pension calculation

To correctly understand minimum pension calculation under 8th CPC, you must be familiar with a few key concepts:

(a) Basic pension

This is the pension amount before adding any dearness relief (DR) or other pension-related allowances. It’s typically 50% of the last basic pay drawn at retirement (under earlier rules). The exact formula may change with 8th CPC.

(b) Fitment factor (multiplier)

A major driver of revision under a new Pay Commission is the “fitment factor” — the multiplier by which the existing basic salary (or pension) is multiplied to arrive at the revised amount. For pensions, the same idea will apply. For reference:

- Under the 7th CPC, the multiplier for salary was 2.57.

- For the 8th CPC, analysts project the multiplier may range between 1.83 and 2.86.

- For pension estimation, many use “Old pension × multiplier = Revised pension”. For example, Old Pension ₹9,000 × 2.86 ≈ ₹25,740.

(c) Minimum pension

This is the floor pension amount guaranteed to a pensioner, irrespective of what they might have otherwise drawn. The 8th CPC may raise this minimum figure as part of its recommendations.

(d) Dearness Relief (DR) or Allowances

In the past, once the Pay Commission is implemented, the existing DA/DR is often reset to 0% and then accrues from there. For pensions as well, DR may start afresh post revision.

(e) Implementation date / effective date

When the new Pay Commission’s recommendations become effective is very important — for salaries/pensions alike. If effective from a given date (say 1 Jan 2026), the pension revision would apply from that date. Some reports indicate that the 8th CPC may be implemented from 1 Jan 2026 (though this is uncertain).

4. Formula for Minimum Pension Calculation (Estimated)

Although exact rules for the 8th CPC are not yet notified, based on historical pattern and current estimates, the formula for minimum pension could be approximated as:

Minimum Pension under 8th CPC ≈ (Existing Minimum Pension) × Fitment Multiplier

Alternatively, or along with this:

Revised Pension = Old Basic Pension × Fitment Multiplier

Many calculators use the second formula for individual pensioners.

Worked Example

Assume:

- Old minimum pension = ₹9,000

- Fitment multiplier = 2.86

Then:

Revised pension ≈ ₹9,000 × 2.86 = ₹25,740 per month. (This aligns with media estimates.)

If a lower multiplier is chosen, say 1.92 (used for some levels in projections) then:

Revised pension ≈ ₹9,000 × 1.92 = ₹17,280 per month. (This is illustrative only.)

Thus, the minimum pension under 8th CPC may lie somewhere in that ballpark depending on what the government finalises.

5. What drives variation in the minimum pension figures?

Several factors will influence how the minimum pension under 8th CPC is actually determined:

(i) Fitment factor decided for pensioners

If the government uses a higher multiplier (e.g., > 2.5) the revised amounts will be higher; a lower multiplier will yield modest increases. The projections vary widely (1.83 to 2.86).

(ii) Whether the minimum pension is reset (floor revised) separately

The Commission may set a new floor minimum pension (e.g., guarantee something like ₹15,000 or ₹20,000) rather than simply multiply the old figure. Some estimates suggest a floor amount around ₹20,500 or more.

(iii) Effective date

If implementation is delayed, the pensioners may wait longer for revision; also, arrears might accrue from the effective date. Accordingly, the real impact on annual pension receipts may differ.

(iv) Impact of DA/DR reset

If DR is reset to 0% at the time of implementation, the first month’s take-home pension might be less than what a simple multiple suggests, until DR accrues again. Historical pattern in past Pay Commissions shows this.

(v) Government policy on other pension benefits

Other changes may affect net pension: commutation factors (i.e., how much you choose to commute and how much pension is left), family pension, whether allowances (if any) are merged, etc.

6. Why increasing the minimum pension matters

- Improve retirees’ standard of living: With inflation and rising costs of living, a larger minimum pension ensures that even pensioners at the floor level have a more dignified retirement.

- Fairness and parity: When salaries of serving employees go up, pensioners expect commensurate revision so their purchasing power is not eroded.

- Fiscal and social impact: Pensioners form a large cohort; higher minimum pensions increase monthly consumption, which has wider economic implications.

- Political and policy pressure: Pensioners’ associations are often vocal about delays and adequacy of pension revisions — so the 8th CPC’s treatment of minimum pension will be under scrutiny.

7. Step-by-step how a pensioner should compute their estimated revised pension under 8th CPC

Here’s a checklist pensioners may follow to estimate what their pension might become under the 8th CPC (once official norms are released):

- Find your current basic pension: For instance, your basic pension (before DR) as on the date of implementation.

- Identify any commutation factor: If you have already commuted part of your pension, your “pensionable amount” will be less.

- Assume a fitment multiplier: Based on media/analyst estimates (say 2.28, 2.46, 2.86) until government finalises.

- Multiply old basic pension × multiplier:

- Revised basic pension = Basic pension × multiplier

- Add/new floor check: If the government specifies a new minimum pension floor (e.g., “minimum ₹20,000”), ensure your calculation meets that.

- Account for DR/allowances reset: Understand if DR will start from 0 on implementation and how it will accrue.

- Check effective date and arrears: If effective date is say 1 Jan 2026, then arrears may be payable from that date to date of payment.

Example

Let’s say:

- Old basic pension = ₹12,000

- Multiplier assumed = 2.28

Revised basic pension = ₹12,000 × 2.28 = ₹27,360 per month.

If the new minimum pension floor is ₹25,000 and your calculated value is above it, you get ₹27,360 (before DR).

Then DR may start from 0% and accrue later.

This gives you an estimated value — actual figures will depend on official govt notification.

8. What remains uncertain and what pensioners should watch out for

There are several variables which are not yet finalized or notified, meaning pensioners must keep track of developments:

- Exact multiplier (fitment factor) for pension revision under 8th CPC.

- Whether the minimum pension will be revised as a floor separate from the multiplier.

- Effective date of implementation of the 8th CPC for pensioners (some reports suggest Jan 1, 2026, others indicate possible delay).

- Whether DR will be reset to 0% at implementation and how it accrues thereafter.

- Whether allowances/benefits will be merged or changed (commutation, family pension, etc.).

- Whether pension increase will be linked to salary increase only, or have a separate formula for pensioners.

Pensioners should monitor government notifications, official resolutions and guidance from the pension department. Acting on speculation alone can lead to wrong expectations.

9. Implications for pensioners: what to plan for

(a) Financial planning

Since a substantial increase in minimum pension is likely, pensioners may need to reassess their monthly budgets. But beware that first month’s take-home may be lower if DR resets.

(b) Taxation and Savings

The higher pension may move you into a different tax bracket (depending on total income). Pensioners should review tax planning, investments, and savings accordingly.

(c) Commutation decisions

If you are yet to retire but expect to benefit from 8th CPC, you may reconsider whether to commute part of your pension. A higher basic pension post-revision may favour lower commutation or different strategy.

(d) Estate/Family planning

Family pension, dependent benefits, etc., might also change — pensioners should plan for succession, will, nominee details.

(e) Stay updated

Consult pensioner associations, official notifications, credible news sources. Do not rely exclusively on speculative calculators — they are indicative only.

10. Summary Table: Key Estimates for Minimum Pension under 8th CPC

| Parameter | Current (Post 7th CPC) | Estimated under 8th CPC* |

|---|---|---|

| Minimum pension (floor) | ~ ₹9,000 | ~ ₹17,000 - ₹26,000+ |

| Multiplier (fitment factor) | — | ~ 1.83 to 2.86 multiplier |

| Revised minimum pension (approx) | — | ₹9,000 × 1.92 = ~₹17,280 |

| ₹9,000 × 2.86 = ~₹25,740 | ||

| Implementation effective date | Already in force | Expected Jan 1, 2026 or later |

* Estimates only—subject to official notification.

11. Why some estimates vary so widely

- Media and analyst estimates use different assumed multipliers (1.92, 2.28, 2.46, 2.86).

- Some assume a separate floor revision in addition to multiplier, some do not.

- Delay in implementation or DR reset can alter real take-home figures.

- Differences in pension categories (whether with commutation or without, number of years of service) may impact actual payout.

- Government may decide different multipliers for different categories of pensioners (e.g., lower level vs higher level).

Hence, you will see a range of numbers in different sources.

12. Frequently Asked Questions (FAQs)

Q1. Will my pension automatically become ₹25,740 if I now draw ₹9,000?

Answer: Not necessarily. That estimate (₹25,740) is based on a multiplier of ~2.86 applied to ₹9,000. The actual multiplier and implementation date are not yet officially notified, so the actual revised amount may differ.

Q2. If I draw more than ₹9,000 now, how will my pension be revised?

Answer: The same multiplier (or formula) will apply to your “basic pension” (whatever you currently draw). So for example if you draw ₹12,000 basic, and multiplier is 2.28 then revised basic could be ~₹27,360. Keep in mind that your commuted pension, family pension, etc., may have separate calculations.

Q3. Will DR (Dearness Relief) continue as before or will it change?

Answer: In past Pay Commissions, when a new commission is introduced, DR is often reset to zero at the start. The 8th CPC is expected to follow similar pattern. So, initially your revised pension may not include DR, and DR will build up thereafter.

Q4. When will the revised pension be payable?

Answer: The effective date is expected to be from the date decided by the government (media speculation suggests 1 January 2026) but an official notification will confirm this. If the rollout is delayed, there may be arrears from interest date to payment date.

Q5. Does this revision affect only central government pensioners or state government too?

Answer: The 8th CPC applies to central government employees and pensioners (under Union Government). State Governments typically have their own pay commissions or may extend similar benefits, but the central scheme does not automatically apply to states unless adopted by them.

13. Concluding Thoughts

The minimum pension calculation under the 8th CPC is poised for a significant revision — with estimates suggesting a potential increase to upwards of ₹17,000-₹26,000 for those currently drawing the floor pension of ~₹9,000. However, these are estimates only, and the final figure will depend on the multiplier (fitment factor) government adopts, the minimum pension floor decided, effective date, and whether DR resets.

For pensioners, it is both an exciting and unsure time: exciting because the prospects of higher pension are real, and unsure because until official notification arrives, you must plan carefully, avoid over-reliance on speculative calculators, and stay updated through credible sources.

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.png)